Despite the global scientific consensus calling for an end to the exploitation of fossil fuels, many new gas extraction sites are being built in Africa. The report lists the new stakeholders, analyzes their projects and puts them in perspective with the challenges of the energy transition.

The report is based on data collected by the Global Oil and Gas Extraction Tracker (GOGET), and its regional counterpart, the Africa Gas Tracker (AGT), launched in 2022 by Global Energy Monitor (GEM). A total of 421 extraction projects have been identified, 84% of them in countries new to the African gas market. They range from pipelines and gas-fired power plants to liquefied natural gas (LNG) terminals and gas extraction sites.

For investment and cost figures relating to these various projects, the report is based on precise data provided by local players, where available, or on rigorous estimates based on the study of regional gas markets. Finally, emissions were calculated using the Oil Climate Index Plus Gas (OCI+) tool.

🔎 Key Takeaways

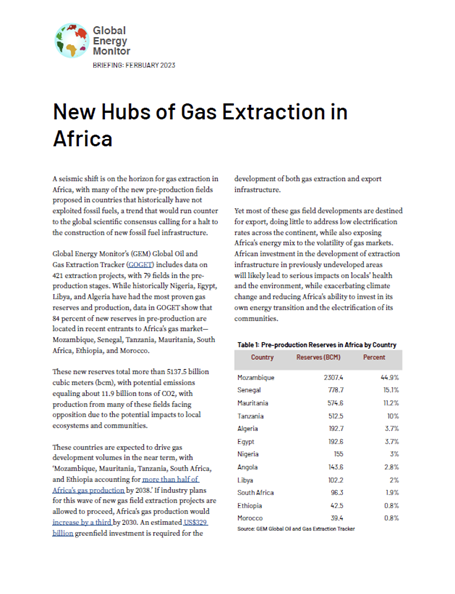

Between 1970 and 2021, 92% of Africa’s gas came from Algeria, Nigeria, Libya and Egypt. By contrast, the continent’s new gas reserves are emerging in new gas market entrants such as Tanzania, South Africa, Mauritania, Ethiopia and, above all, Mozambique. The report suggests that these five countries could account for more than half of Africa’s gas production by 2038.

These reserves, representing more than 5,137.5 billion cubic meters (bcm) of gas, would increase the continent’s gas production by a third by 2030, and emit more than 11.9 billion tonnes of CO2.

Capital expenditure on the various LNG terminals under development would amount to $103 billion.

97% of new LNG infrastructure is earmarked for export, mainly to the European Union, which is looking for sources outside Russian gas.

The main companies owning reserves in new African gas sites are owned by European, North American and Asian players, and the vast majority are headquartered in Europe (the most influential being BP and TotalEnergies).

Most of the benefits of these projects will not accrue to Africa: its energy mix risks becoming dependent on the gas market; its electrification rate could remain low, even among the new gas producers (only 30% of the Mozambican population have access to electricity); the continent’s capacity to invest in its own energy transition will not increase; local ecosystems and communities risk being impacted by these large-scale projects.

💡 For a more in-depth look at gas in Africa, the Gas for Africa Report 2023 published by the International Gas Union (IGU) takes stock of the continent’s potential, and provides an understanding of the issues of sovereignty, development and their relationship to the dynamics of energy transition.

By continuing your visit to this site, you agree to the use of cookies for audience measurement purposes.